In this Melbourne Real Estate News Update:

- Ticker Property – Real Estate TV with Mark Errichiello Director of Master Advocates Real Estate Services

- Coronavirus: COVID19 Update – Real Estate Practices

- REIV VIC Report and CoreLogic and Herron Todd White Residential/Commercial National Market Outlook from March 2020 Research QTR

- Coronavirus: An overview of measures put in place by some service providers, government bodies and the REIV

- Coronavirus (COVID19) latest Coronavirus news, updates and advice from government agencies across Australia

- Moonee Valley City Council business updates – Economic Development E-connect Newsletter

- Comments on the market and COVID19 – NSW and Australian Buyers Agent of the Year – Rich Harvey CEO & Founder, Property Buyer

- CoreLogic Eliza Owen – Coronavirus And The Australian Property Market

Ticker Property – Real Estate TV

Host: Kris Bondin CEO of Moving Hub with Mark Errichiello Director of Master Advocates Real Estate Services

Ticker Property

www.tickertv.com.au

Master Advocates – Real Estate Services Pty Ltd

While we all face these challenging COVID19 times together, trying to keep safe and healthy, working remotely and working from home. This interview was no exception. It was a pleasure to discuss and share some opinions on some of the effects on the real estate practice and the options to navigate the situation we find ourselves in. This effects everyone as we are one community and we all need a roof over our heads, tenants, landlords, buyers and sellers.

Happy to provide complementary advice on a detailed level and consultation for any individual needing real estate advice and sharing of opinions should they wish to reach out to us with public or private messages or simply want to talk and ask a few questions on the phone.

Warm regards and be safe.

9379 1919

0408 988 118

Mark & Michelle Errichiello

Licensed Estate Agents, CEA (REIV)

Buyers Advocacy – Property Management – Vendors Advocacy

www.masteradvocates.com.au

Watch the full interview with Mark Errichiello of Master Advocates on Ticker Property TV:

Coronavirus: COVID19 Update – Real Estate Practices

The REIV have shared further clarification regarding new restrictions on Open For Inspections and Auctions.

Prime Minister Scott Morrison announced new limits on gatherings. The announcement stated that open house inspections, auction houses, gatherings in auction rooms and real estate auctions can no longer continue.

REIV received clarification from Consumer Affairs Victoria on the scope of these restrictions:

• Inspections by appointment for sales and rentals can continue

• Auctions via online remote and digital methods can continue

CAV will be notifying all real estate agents on all Government directives and updates as soon as possible.

Please note, the restrictions announced are to limit public gatherings and not the business of real estate. As real estate agents it is up to us to use best judgement and avoid unnecessary in-person interaction as far as possible.

No further information has been provided at this time regarding leases.

The Premier has stated that further restrictions are expected in the near future. The situation continues to evolve so it is important that we continue to work together and review our work practices and monitor the advice daily.

We at Master Advocates understand how stressful this can be on the community and property buyers, vendors, tenants and landlords, though we are here to support you as our clients as much as possible. Our office is currently closed to the public, however we are still onsite working from our office or offsite from home and arranging online video conference meeting and essential meetings one to one in person if required.

We must be mindful and prepare ourselves if we need to

operate offsite completely. Thankfully our office adopted technology early and resources that allow us to operate on electronic systems, including majority of services being capable to be managed offsite effectively and efficiently. So we are still here to help no matter what may come. This includes being engaged as your advocates across Buyers Advocacy, Property Management and Vendors Advocacy as required on REIV Authority to act and limited Power of Attorney specific to individual property, for example remote and online auction bidding to act on your behalf and be present during property inspections and or on site to execute documentation and bidding if permitted and required.

As a local business we had already decided to limit the number of non-essential gatherings by not conducting any further public open for inspections and auctions and put this into action earlier this month.

This is the best option moving forward to keep our staff, clients and community safe during this unprecedented time for not only Australia but the world.

We are keeping up to date with our governing bodies, Consumer Affairs Victoria, the REIV and both the state and federal government to make sure we are taking proper precautions and maintaining sanitary recommendations and social distance directives.

However we will be still conducting private appointments for our properties which we are prospecting to purchase and properties for lease on behalf of our clients, but conditions of entry apply, you will be required to register with our

Covid-19 consent form and/or questions based on conditions of entry prior to entering the prospective property and/or office so we can make sure it’s a safe environment for everyone involved.

Please keep to the health and safety practices that have been outlined regarding social distancing and safe health practices (subject to change as directed by government on a daily basis).

If there is any questions or concerns that you have please contact us to clarify.

We are taking all steps to protect our staff and thank you for your cooperation, patience and great work ethic at this very trying time. It is appreciated.

Inspections in Vacant and Occupied Properties:

Important Update, REIV latest update on advice and government directives for real estate agents as of today Thursday 9th April 2020.

We have received new advice from the Office of the Minister for Consumer Affairs regarding the restrictions on inspections. This advice has been provided after consultation with the DHHS. Their advice conflicts with the guidance on the CAV website.

Please review and implement this advice with immediate effect.

NOTE: The restrictions vary for Vacant and Occupied properties and are based on the Stay at Home Directions and Restricted Activities Directions (New Directions)

VACANT PROPERTIES

Under the New Directions, an estate agent can only organise private appointments for in-person inspections of residential properties.

Practically, this means an agent can conduct a private inspection of a vacant residential property for potential purchasers or potential tenants provided that only one potential purchaser or potential tenant is in attendance, or if there is more than one potential purchaser or potential tenant in attendance, those people ordinarily reside in the same premises (i.e. if they were a couple or family that lived together).

OCCUPIED PROPERTIES

The conflicting advice that we received suggested that agents must no longer conduct public or in-person private inspections of tenanted or occupied properties. This is inconsistent with the CAV website, which only encourages that these do not occur.

The REIV recommends that good real estate practice would dictate that private inspections of tenanted properties should not occur. The situation is different for properties for sale where the vendor occupies the premises and is likely to be more cooperative. In order to comply with the legal requirements under the New Directions the inspection should be timed to coincide with the absence of the vendor for one of the allowable reasons: shopping, work/education, health or exercise. There is no exemption for tenants or occupants to temporarily vacate their place of residence to facilitate inspections, therefore, obtaining the cooperation of the vendor in conducting the inspection will be vital.

Alternatively, during the Stage 3 restrictions, vendors or landlords wanting to conduct inspections of tenanted properties can do so via virtual inspections, or wait until the property is fully vacated and disinfected.

For the purposes of filming a virtual inspection, agents can alone attend an occupied property as long as they comply with the requirement that only one person can enter a place occupied by persons who reside in the same premises and all other requirements relating to social distancing, cleaning and hygiene.

We understand that this advice significantly impacts all real estate businesses but it is important to focus on the outcomes, we can still trade unlike many other industries. Many agents have already adopted technology and we recommend all Members consider the options available. Some providers you may want to consider are listed here.

Based on feedback and further consideration, templates provided for managing rental assistance requests from residential tenants have been updated and available to REIV members.

We are currently working through the information on Commercial Tenancies and will provide further updates and tools as soon as possible.

Stay safe, stay healthy and have a good Easter break.

The above update was kindly provided by the REIV President Leah Calnan

DISCLAIMER

The REIV gives no warranty about the accuracy, completeness, or reliability of the content. The content is for general information only. It is not advice or intended as advice and in no circumstances should be relied upon as such. Readers and third parties should verify the content and seek their own independent advice before making any decisions, financial or otherwise. The REIV does not endorse or take any responsibility for material on third party websites referred to in this information.

REIV VIC Report and CoreLogic and Herron Todd White Residential/Commercial National Market Outlook from March 2020 Research QTR

If you’re interested in the market outlook, the attachments are a good collection of property data reports. Most data reporting is generally a few months behind based on settled property, but these seem more up to date with February and early March records.

Herron Todd White Residential month-in-review-march-2020

Herron Todd White Commercial month-in-review-march-2020

CoreLogic RP Data home-value-index-march-2020

REIV research-bulletin-march-2020

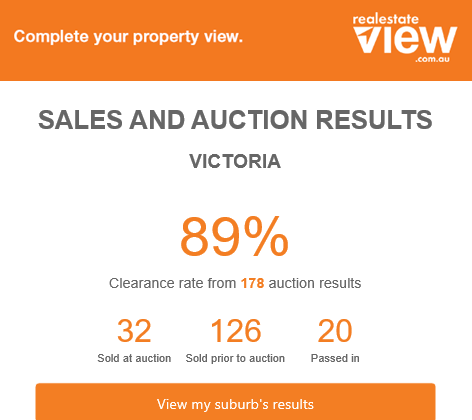

Victorian Sales and Auction Results – Suburbs

My opinion, despite being what was seeming to be a strong bounce back phase early 2020 after the decline in the market of 2018 and 2019 post the financial services and banking royal commission in Australia. We still had a positive buyer sentiment but now with the global economic uncertainty with the effects of the Coronavirus, many buyers and lending institutions are starting to feel cautious and somewhat scared to invest in the event of a global recession or even worse depression. Some buyers are sharing articles such as the below when asked why they are not ready to make offers or decisions to buy right now in the short term or over extend themselves purely on expected sale asking prices. The demographic of buyer and seller types will change over the coming months, the buyers with pre-approval of finance lending or extra cash to take advantage of fair market prices and the sellers that are motivated to sell at a fair price though still able to hold in the market without being forced to sell at rapidly reducing market prices with the exception of a few distressed sales with vendors that can no longer hold for a better price expectation or without access to additional savings that will emerge and buyers taking advantage of these situations over the next few months. The exeption is that this will happen, but the majority of sales values in the well established suburbs will not be effected long term.

It is common for estate agents to get excited about high clearance rate property sales and interest rate cuts by the RBA if the major banks pass on the saving. Now as of Tue 3rd March and 7th April 2020 we have reached a historical low base rate, cut down by the RBA and some economists suggesting you should now be able to secure interest rates on mortgages with banks sub 3% if buying or refinancing. It is important to note that the volume of sales recorded with the high clearance rate of motivated and realistic sales during the past few weeks have been recorded on a low level of listings in the market, approximately 178 auction results when in an average market with a healthy consistent level of listings, there should be at least 1,000 to 1,400 recorded auction results any given week. During the climate of COVID19 and mortgage lending serviceability criteria and responsible lending conditions, more sales will most likely refer to private sale by negotiation rather than online remote bidding auction environment without any public gathering.

The RBA and Government don’t cut rates in a rapidly growing economy. They certainly don’t cut rates this low unless there is cause for concern and urgent need to stimulate the economy to spend. Sadly with fear of a recession most buyers are retaining the interest rate saving rather than spending more or competing with other buyers to purchase property. Best case scenario we hold property value at current levels within a 20km radius of the Melbourne CBD and established suburbs.

There is likely to be a short term decline in property prices this year rather than any growth, with the hope that once the effects of the coronavirus are clear and no longer impacting the property market sentiment we return to a steady and sustainable capital growth cycle.

Melbourne population growth and demand to own property in the world’s most liveable city will always prevail long term, especially with uncertainty in the share market, we should have greater long term demand in our more consistent and reliable asset class being property.

Melbourne is set to become the country’s most populous city by 2026.

The rise of the Victorian capital is shaping up to be the social and economic story of the 21st century, forcing us to change the way we think of ourselves as Australians.

Melbourne can more easily add new suburbs to its metropolitan fringe than the landlocked Sydney, and housing remains 22 per cent cheaper.

Greater Melbourne grew by one million people between 2008 and 2018, pushing its total population past 5 million as the nation’s crossed 25 million. Sydney added just over 800,000 people over the same period to reach a population of 5.2 million, while Brisbane’s population increased by 450,000 to 2.5 million.

Those raw numbers actually understate the shift. Melbourne is growing at a faster rate than any capital or regional city in the country; faster even than the booming coastal settlements north and south of Brisbane. Gaps that were once thought permanent between Melbourne and Sydney, and between Melbourne and Queensland, are suddenly closing.

A decade ago, Sydney still had 450,000 more people than Melbourne, while Queensland’s advantage was 300,000. This year, Melbourne will be larger than all of Queensland, and barring an economic catastrophe, it should pass Sydney before the end of the 2020s, reclaiming the title of our most populous city, which it last held in 1901. On current trends, the handover will occur around 2026.

Victoria’s Big Build: Major road and rail projects now in planning and construction

Thankfully business as usual for the most part of operations in real estate, with the age of information and technology innovations, most of our tools and resources make it possible for us to conduct our business with cloud based online services and electronic certified software for transactions if necessary. On site inspections and deals with properties are still being completed currently, business as usual with a higher regard and caution for social hygiene.

Mark Errichiello

Director, Licensed Estate Agent, CEA (REIV)

Master Advocates – Principal Buyers Agent

Coronavirus: Update

An overview of measures put in place by some service providers, government bodies and the REIV

| VCAT

In the interest of public safety and in an effort to implement social distancing measures, VCAT has moved to conducting hearings by telephone. As a result, VCAT venues will be closed to the public until further notice. · Face-to-face hearings, and all non-critical matters have been adjourned for the time being · Residential Tenancies and Guardianship matters (and a small number of other critical matters) will be heard by telephone. VCAT will contact impacted parties regarding their matters · VCAT is still conducting its work and users are encouraged to contact 1300 01 8228 to discuss their matters. Follow VCAT News for updates. |

Government agencies and other service providers

· Realestate.com.au : The REA Group has advised agents of the measures they are putting in place like re-loading any listing that has been taken off the market at no charge to the vendor/agent, extending the listing duration should a property fail to sell in the initial duration and deferring rate increases. Please contact them directly for further information. |

Other recent articles published in the past 30 days to keep up to date with and understand what information and opinions buyers, sellers and consumers are being exposed to:

https://www.rba.gov.au/media-releases/2020/mr-20-06.html

https://www.rba.gov.au/media-releases/2020/mr-20-11.html

https://www.rba.gov.au/media-releases/2020/mr-20-12.html

https://www.abc.net.au/news/2020-03-13/coronavirus-stimulus-package-lessons-from-gfc/12052270

Coronavirus (COVID19) latest Coronavirus news, updates and advice from government agencies across Australia

Coronavirus (COVID19) Australian Government

COVID19 Australian Taxation Office

Coronavirus information and support for business.gov.au

COVID-19 (Coronavirus) resources for business Victorian Chamber of Commerce and Industry

Australian Government Department of Health

https://www.health.gov.au/

coronavirus-covid-19-at-a-glance-coronavirus-covid-19-at-a-glance-infographic_3

Moonee Valley City Council business updates – Economic Development E-connect Newsletter

On a local level Mark Errichiello has been involved with the local traders of Essendon for several years and is the current Chairman of the Essendon North Village Traders Association representing over 165 traders in the community that are all experiencing tough times at present and what we will all face together that is still to come. Now more than ever it is important to shop and support local, despite COVID19, many local businesses have adapted to take away and online remote shopping for products and services. Love your local village now is a phrase with more significance so that once we make it through to the other side of this, our greatly loved and appreciated local businesses and traders that make our great local community culture are still there for us all to enjoy and support.

Moonee Valley City Council business updates. Our E-connect Newsletter aims to provide business support and continuity through the global COVID-19 pandemic.

Subscribe here to receive our E-connect newsletter and Business Alerts

What you will receive:

E-connect newsletter. Currently distributed weekly (during COVID-19 State of Emergency) support and advice to business in easily navigable links, includes useful business information such as webinars, business grants, and tips and tools to help your business. Business Updates timely, brief update emails on important changes or information as they arise.

The Moonee Valley Council have already been hosting weekly webinars to keep in touch and assist local businesses keep informed and aware of subsidies that are now available to them via government.

• Outline of the Current Stimulus Packages available

• Effect on different business structures

• How to access the Packages

• Sole Traders – what’s available for you

• Casual Workers – what’s available for you

• Working from home

• Think outside the box

For more information about other support from Council during this difficult time please see the MVCC COVID-19 Business support webpage. The business community can make direct contact with the Economic Development team via business@mvcc.vic.gov.au or 9243 8866 to seek further support or information.

City of Moonee Valley E-Connect Registration

Warm regards

Julie Stevens

Business Development Officer

Phone 9243 1038 | Email jstevens@mvcc.vic.gov.au

#LoveOurLocalVillage

#ShopLocal

#SupportLocalTradersandFamilies

ENV Traders Association Chairman

Mark Errichiello

NSW and Australian Buyers Agent of the Year – Former President Real Estate Buyers Agent Association of Australia

Rich Harvey CEO & Founder, Property Buyer

What Rich Harvey says about Master Advocates: “Mark Errichiello is a long term colleague and fabulous buyers advocate that has assisted many of our Melbourne based clients in the past.

He and his company have excellent connections to find you a suitable property to match your budget and requirements. (Mark also assisted me with research for the Buying Blind TV series!)”

Rich Harvey Property Buyer:

To get a sense of what might happen, it’s important to reflect on what has happened in the very recent past.

Right now, forgetting the uncertainty of the coronavirus pandemic for a moment, ask yourself a question.

If you could go back in time 30 years, would you take the opportunity to invest money in Sydney’s or Melbourne’s property market?

I doubt you’d find many people who wouldn’t.

Price growth over the past 30 years has been strong, steady and resilient. That’s despite a series of significant events that caused extended and painful bloodbaths in other markets – shares, foreign currency and resources.

I’m talking about the recession in the early 1990s, the dotcom bubble collapse in the late 1990s, the September 11 terror attacks in 2001 and the outbreak of the SARS virus in the mid-2000s.

What did property do in all of these major, scary, disruptive and devastating events? It grew in value.

Let’s take a look at an example of this. Property prices during the big one – the Global Financial Crisis.

What happened after the GFC?

We all remember the impacts of the Global Financial Crisis, right? It was a scary time for investors of just about any ilk, as the share market posted heavy losses and spilled red all over the top end of town.

But do we really remember what happened to property? Ask most people and they might recall it being a pretty dire time for those who put their cash in bricks and mortar.

But it wasn’t. I personally bought two properties that year that have done exceptionally well.

Buying during the GFC proved to be one of the best times to get onto the ladder.

There were dips, for sure. The national median house price fell by 3.5 per cent over two consecutive quarters at the height of the panic in late 2008. But then… they rose from early 2009 on the back of government stimulus. And the turnaround was sharp.

Within a quarter, the market had made up all of that lost ground and in the two quarters after that, had increased by about seven per cent.

And the upward trajectory continued.

As Domain summarised in a recent article: “It was home owners bold enough to strike during the global financial crisis who made the biggest windfall.”

Those investors saw the opportunity to act in a market with exceptional long-term growth prospects, underpinned by a long-term supply and demand imbalance, and to do so with a bit less competition while buyers were running scared.

A contributor to an increase in activity was falling interest rates. The cheap cost of credit encouraged people to act while the buying was good. We’re in a similar scenario already, with record-low rates significantly boosting borrowing power and lowering costs.

Another major contributor was that the government sought to head off an economic mess by pouring billions and billions of dollars into a number of key battlegrounds. Guess what Scott Morrison is about to do?

The value of stability

One of the things I think we’ll see over coming months is a resurgence in the property investor market.

Those types of investors have had a rough time on the share market, thanks to coronavirus and international market slumps. They’ll want to put their money in an asset that’s shown to perform well through historic rough patches.

Coronavirus And The Australian Property Market

https://www.corelogic.com.au/news/coronavirus-and-australian-property-market

The Corelogic Datasets Capturing The Coronavirus Shift

Keeping up with institutional responses to COVID-19

Coronavirus And The Australian Property Market

17 Mar 2020

Amid the spread of coronavirus, the past few weeks have seen increased expectations of an Australian recession, a slowdown in business activity and trillions of dollars wiped off global share markets. It has many asking what the impact of the coronavirus would be on Australian residential property.

This note explores fundamentals of housing to better understand outcomes in the current climate. It is found:

- Housing has performed relatively well against negative economic shocks, but the unique conditions of a pandemic-induced economic slowdown must be considered;

- Housing is an illiquid asset and a consumption good, which shows far less volatility and decline than share markets;

- In the coming weeks, property transactions may fall significantly, but the impact on values is unclear; and,

- Existing economic headwinds, including high household debt, make the property market particularly susceptible to a fall in demand. However, Australia does not have ‘one’ property market, and a decline in demand will be tempered by the composition of the local workforce, and the state of household finances.

Australian residential property has historically fared well against negative economic shocks

In beginning to assess the impact of the current slowdown on property, it is worth exploring how property has historically responded to negative economic shocks.

Major share market losses and recession are not necessarily predictors of declines in housing values. This can be seen in the figure below. When significant, negative economic shocks occur, the effect on the housing market varies. Property value changes depend on the level of impact on Australian industry.

As an example, the 1987 ‘Black Monday’ stock market crash was a negative shock, in which the Australian share market lost approximately 23% of its value in a single day.

But housing values were largely unaffected. By October of 1988, residential property values experienced double-digit growth, as financial deregulation contributed to asset value inflation.

In the 12 months to January 1988, the Australian unemployment rate declined 60 basis points. The Hawke government also reinstated negative gearing as we know it today, after temporarily quarantining any losses associated with rental property between 1985 and 1987. This may have provided an extra boost to Australian property investment at the time.

By the early 1990’s, Australia experienced a recession and property values declined, but only by -4.4%, from June 1989 to October 1990.

In 2007-08, when the GFC began, the Australian economy was more globalised. A slowdown in the global and domestic finance sector affected employment, incomes and subsequently borrowing capacity for housing.

The national dwelling market declined -7.5% from February 2008 to January 2009. However, an uplift in mining-related investment, the start of a rate cutting cycle and government stimulus saw a fairly swift recovery.

Recently, values been more reactive to structural changes in the lending space. Between 2014 and 2017, a series of policies limiting investment housing lending catalysed one of the largest and longest property market downturns since the early 1980’s. However, further rate cuts and eased serviceability assessment prompted an owner-occupier led rebound.

The share market and housing market perform differently

Aggregate figures on the housing market suggest that the slowdown in economic activity from the coronavirus has not impacted housing markets in the same way as equities. This is nothing new. Historically, comparing the S&P ASX 200 index with the CoreLogic home value index, suggests that property responds to macroeconomic conditions at a lag, and avoids the same extent of decline or volatility.

There are a couple of reasons for this:

- The relative illiquidity of housing (high transactional costs and long settlement periods) means it takes longer for property to transact, which makes ‘flights to’ or ‘sell-offs’ of property less likely amid economic uncertainty; and,

- Housing is used as a consumption good, and is less likely to be speculated upon relative to equities.

The latter point is a particularly insulating factor at the moment. Since the start of the property market upswing in June 2019, investors comprised 28.2% of the new finance taken out to buy property. This is down from 39.5% in the previous upswing.

In other words, the retreat of investors from residential property will not have as large an impact as it would have two years ago.

The relatively low levels of foreign interest in the Australian dwelling market over 2019 also means there is less risk to the market from declines in this buyer group. According to the latest NAB residential property survey, foreign buyers in the December quarter of 2019 made up 7.0% of new property purchases (down from the survey average of 10.2%), and 3.8% of established property (down from the survey average of 6.1%).

Some will be exposed to a downturn in international market participants from travel bans. These include new unit projects targeting foreign buyers, and landlords who are reliant on foreign students or tourists for rental occupancy.

Property is not completely insulated from economic events. Depending on the extent of spread of coronavirus and institutional responses, reduced business activity could materially slow the flow of income and credit. This would have significant impacts for the property market.

Sales activity likely to decline, while the impact on values is less clear

Property transaction volumes are likely to fall in the coming months, but the outcome for values depends on temporal expectations around coronavirus, and longer-term employment conditions.

In the short term, the coronavirus and subsequent share market declines have already had a significant impact on consumer confidence. This may lead to postponed dwelling purchases, as housing is an expensive, high commitment purchase decision.

The Westpac-Melbourne Institute Consumer Sentiment Index declined -3.8% over March to a 5 year low, and recorded the second lowest reading since the GFC. The index is still 15.3% higher than the level at which it bottomed out in 2008, suggesting consumers are less worried about the economy than at the GFC.

Interestingly, the ‘time to buy a dwelling’ index component only fell -0.3% in March, but declines may soon deepen. The ‘house price expectations’ sub index fell more sharply, down 6.6% in March. This was the largest fall since February last year.

A more direct impact on transactions could be the rise of isolation precautions. If Australian governments follow quarantine measures enforced in Italy and China, then inter-city travel would be restricted, and confinement to the home would prevent physical inspections and on-site auctions.

While this may seem extreme, it is not unlikely: Victoria and the ACT have declared a state of emergency across the regions, increasing power of health ministers to enforce self-isolation.

This presents a challenge to the real estate sector, which often necessitates physical inspection of property and, in the case of auctions, bidding environments involving groups of people.

Real estate industry professionals may respond by offering private inspections rather than open homes, virtual inspections using technology, or remote auctions. But such technologies can be difficult to adopt in the best economic conditions. Prospective buyers and sellers are likely to postpone activity until conditions revert to normal.

Property values may not be impacted the same way. One important facet of the unfolding economic slowdown, is that it is led by institutional responses to the coronavirus pandemic. This is a unique cause for halting production and consumption.

Vendors may view the current pandemic as a temporary economic condition. If monetary and fiscal stimulus can adequately support business and household income amid the slowdown, then the next few months could see a sharp contraction in sales volumes, but not necessarily dwelling values.

This is because the expectation would be for market activities to return. Influenza periods for example, typically last 3-4 months. It is unclear whether coronavirus will be seasonal, but, after mass quarantines, China is now showing a slowed spread of the coronavirus. South Korea is also seeing a drop off in new reported cases after a social distancing campaign.

A comparison may be drawn with the high seasonality in sales volumes usually seen around annual holiday periods. Over the past two decades, the decline in sales volume activity from the month of November to December averaged -15.9%, and sales volumes in December have a seasonal factor of 0.9. By comparison, the past two decades have seen an average 0.2% uplift in values from November to December, with very little seasonality present.

While the current pandemic is by no means a holiday, it is temporary. Unless the current slowdown presents a significant drag on incomes, vendors may not see the need to lower their property value expectations.

Headwinds for housing demand

In the long term, housing market values and activity will be linked to the extent that quarantine measures affect income, employment, borrowing capacity and credit availability.

The largest and most direct industry shocks from the coronavirus are expected in:

- tourism, where increasingly strict quarantine procedures deter travel;

- education, due to fewer foreign students being able to travel;

- hospitality, where social distancing leads to a decline in café, bar and restaurant visitation;

- retail, which will be dragged down by low consumer confidence levels; and,

- arts and recreation, where visitation to theatres , cinemas and art galleries are already on the decline.

GDP growth in the March quarter was initially expected to be about 50 basis points lower from what it otherwise would have been. But research on the impact of past influenza pandemics suggests the losses may be greater.

Unlike the global financial crisis, where a mining boom, as well as monetary and fiscal policy were effective in helping Australia avoid recession, the domestic economy now faces new challenges:

- Australia is not expecting another mining boom. GDP figures for December show that mining investment is 19.7% lower than where it was at December 2008.However, the RBA are confident in an uplift in the sector over the year, and note that commodity prices have been fairly resilient amid share market declines.

- There is ongoing weakness in the private sector. Annual changes in private sector spending have been negative since June 2019. This has knock-on effects for employment and income growth, which in turn limits borrowing capacity for property.The recently announced stimulus package handed down by the Morrison government goes a long way in targeting businesses investment, with up to $25,000 available for small to medium enterprises, apprenticeship wage subsidies and an increase in the value threshold for instant asset write offs to $150,000.

- There is less room to reduce the cash rate. During the GFC, the RBA implemented 6 rate cuts, taking the official cash rate from 7.25% in August 2008 to 3% by April 2019.Currently, the cash rate is a record low 0.5%. Market expectations currently indicate with certainty that there will be a 25 basis point cash rate reduction in April.There is not much ammunition left in monetary response, apart from pursuing a quantitative easing strategy. The RBA has indicated they will commence bond purchases and repurchasing operations, which involve on selling government bonds to investors before buying them back at a higher price.

- Household debt is near record highs. Household debt is closely monitored by regulators. September quarter data suggests that both total household debt to income, and housing debt to income, are just below the record highs in the June quarter.At September 2019, total debt to household income was 186.5%. This was mostly comprised of housing debt to income (141.3%). The loss of jobs amid a business slowdown could increase the incidence of non-performing loans, especially since the latest APRA data suggests that an increasing portion of finance (38.6%) is being lent with a loan-to-value ratio of over 80%.Given the high levels of housing debt in Australia, it is important to consider the risk of increased non-performing loans in the current environment. RBA research suggests that at December 2017, about one third of owner occupier loans had at least a two year buffer in mortgage repayments. However, around one quarter had less than one month’s buffer.If social distancing measures are in place for an extended period of time, those more vulnerable households at risk of mortgage stress could require targeted intervention to avoid delinquency.Despite these fragilities, and a technical recession increasingly likely, there are some safeguards that will lessen the blow of a halt in income and employment, and the availability of credit.

Just days after announcing its $17.6 billion stimulus package, the government is considering a second stimulus package.

On Monday the 16th, the council of financial regulators announced further supportive measures for credit availability, including the RBA preparing the start of quantitative easing, and APRA have announced the potential easing of regulatory requirements to support the flow of credit.

In an address on the 11th of March, the RBA was keen to emphasise that the virus is ultimately a temporary disruptor to business activity, and that eased monetary conditions and fiscal policy would help the economy to “bounce back quickly once the virus is contained”.

Not all markets will be equally impacted

Importantly, Australia does not have ‘one’ housing market. While this note considers the residential market in aggregate for simplicity, economic downturns have certainly created more acute, localised declines in property, such as;

- The collapse of mining related infrastructure projects in 2014, which still see Darwin property values more than 30% below the record high;

- Over-supply in the Brisbane unit market, where the latest data shows values are still -11.2% below the record high; and,

- The impact of extreme weather, storms and flooding, which has suppressed property price growth in far north Queensland.

Given the idiosyncrasies of the current downturn, there are likely to be parts of Australia where housing demand, including rental demand, will fall more sharply than others.

These include areas where workers cannot perform their jobs remotely, and may have to sacrifice income if social distancing is enforced, where there is a high incidence of casual employment, and where there is a high concentration of employment in affected industries.

Looking at the concentration of the workforce in accommodation and food services for example, points to pressure on households in Sydney’s Inner West, which has the highest portion of workers employed in this sector by SA4 region (12.7% at November 2019).

Conclusion

The coronavirus outbreak clearly presents some downside risk for the Australian housing market, but ultimately, the impact remains highly uncertain. New information and policy responses are unfolding daily, making it impossible to provide a reasonable forecast of capital growth. Some added context however, is remembering the fundamentals of the property market, and idiosyncrasies of a pandemic-led downturn.

Property is less volatile and slower to respond to market shocks than equities, it is a consumption good and it is tied to fundamentals of employment opportunity and income growth. In the current climate, the Australian housing market is more insulated from foreign demand and investment speculation than it has been over previous years.

Transaction activity is likely to be impacted more than market values. As consumer confidence reduces, and labour markets are disrupted, more Australians are likely to put high commitment decisions on hold until there is more certainty around the economy, jobs and household finances.

Additionally, stimulus measures including emergency level monetary policy settings and a surge in fiscal spending should help to cushion the impact of reduced business activity, but a recession in the first half of 2020 still looks likely.

The current high level of household debt amplifies the risk of unemployment on housing market conditions. However, areas severely impacted by social distancing would be less resilient than others in rebounding from the coronavirus pandemic.

Our views and research on the market outcomes in relation to the coronavirus will continue to evolve as more information comes to light.

Information sourced in this news update: 7News, ABC News, RBA, Consumer Affaires Victoria, REIV, CoreLogic RP Data, Herron Todd White Residential/Commercial National Market Outlook, Rich Harvey Property Buyer, Ticker Property TV, Kris Bondin Moving Hub, Mark Errichiello Master Advocates