Why buyers, investors and professional advisers must follow the money before following the advice

In this edition of Master Advocates News:

- Why buyers, investors and professional advisers must follow the money before following the advice

- VICTORIAN GOVERNMENT AUCTION RESERVE PRICE DISCLOSURE LEGISLATION – VIC GOV Media Release and the REIV Response

By Mark Errichiello | Master Advocates – Real Estate Services Pty Ltd

Why this matters now

Property markets have a way of revealing the difference between genuine advice and sales activity dressed up as advice.

Whenever markets turn, interest rates shift, tax settings change or regulation tightens, highly polished property offers often begin appearing through referral networks, professional adviser databases, investor webinars and so-called research briefings. Some may be legitimate. Others may operate more like product distribution channels, where the client is being guided toward a pre-arranged property solution that generates commissions, rebates or referral income for parties behind the scenes.

The language can sound sophisticated: tax benefits, negative gearing, capital gains tax, new build opportunities, national research, hotspot forecasts, investor-grade property and access to exclusive stock. Those topics can be relevant. But they should never replace the most important consumer questions: who is providing the advice, are they licensed and qualified to provide it, who is paying them, and whose interests are they legally and commercially acting for?

A tax change is not a property strategy

Tax settings can influence timing, ownership structure, cash flow and investment modelling. They should be considered carefully with appropriately qualified tax and financial advisers. But tax should never be the only reason to buy a property.

A property still has to stand on its own fundamentals: location, land value, construction quality, scarcity, resale demand, tenant appeal, holding costs, planning controls, title structure, strata or owners corporation risk, future supply, lending conditions, rental sustainability and realistic exit options.

Buying a weak asset for a perceived tax outcome can leave buyers with the worst of both worlds: poor capital growth, limited liquidity, weak rental demand, settlement risk, building defects, high holding costs and a long path back to financial strength.

Are your advisers licensed, qualified and acting within their authority?

Before relying on property, tax, financial, credit, legal or investment-related commentary, consumers should ask whether the person giving that advice is properly licensed, qualified and legally permitted to provide it.

A licensed buyer’s agent is not automatically licensed to provide tax, financial product, credit, legal, accounting, SMSF or trust-structure advice. Likewise, an accountant, mortgage broker, financial adviser or other allied professional is not automatically licensed to act as a property buyer’s agent, sell property, recommend a specific property product or receive property-related commissions.

Depending on the practitioner, their licensing category, professional standards, legislative obligations and regulatory body requirements, some advisers may be restricted or strictly prohibited from receiving a share of commission, rebates, referral fees or other benefits from allied industry referral partners. This is not a technicality. It goes directly to independence, conflicts of interest and the client’s ability to trust the recommendation.

The warning sign: advice that starts with the product, not the client

A genuine independent buyer advocacy process should begin with the client: their budget, borrowing capacity, risk profile, family circumstances, lifestyle needs, investment horizon, cash flow tolerance and long-term goals.

A conflicted process often starts somewhere else. It begins with a stock list, a project pipeline, a developer relationship, a builder relationship, a referral agreement or a commission arrangement. The buyer is then matched to the product, rather than the property being tested against the buyer’s best interests.

This distinction matters. A buyer’s agent paid by the buyer should be free to assess the whole market and advise against a purchase when the evidence does not stack up. A so-called “free” or vendor-paid model may look attractive on the surface. But if the seller, developer or builder is funding the commission, buyers should carefully ask whether the representative is truly independent or effectively acting as a selling channel.

Follow the money and you will often find the motivation

The clearest consumer protection question is simple: who gets paid, by whom, and when?

If a property adviser, buyer’s agent, accountant, financial adviser, mortgage broker, referrer, educator, marketer, developer, builder or selling agent receives a fee, rebate, referral payment, commission, marketing allowance, trailing benefit or other commercial benefit, the buyer should know that before relying on the advice.

A disclosure buried in fine print is not enough. Consumers should ask for clear written disclosure identifying every party receiving money from the transaction or referral pathway. This includes rebates, referral fees, developer commissions, project marketing fees, lead-generation payments, buyer’s agent fees, sales commissions and any other benefit connected to the recommendation.

What experienced independent buyer advocacy should look like

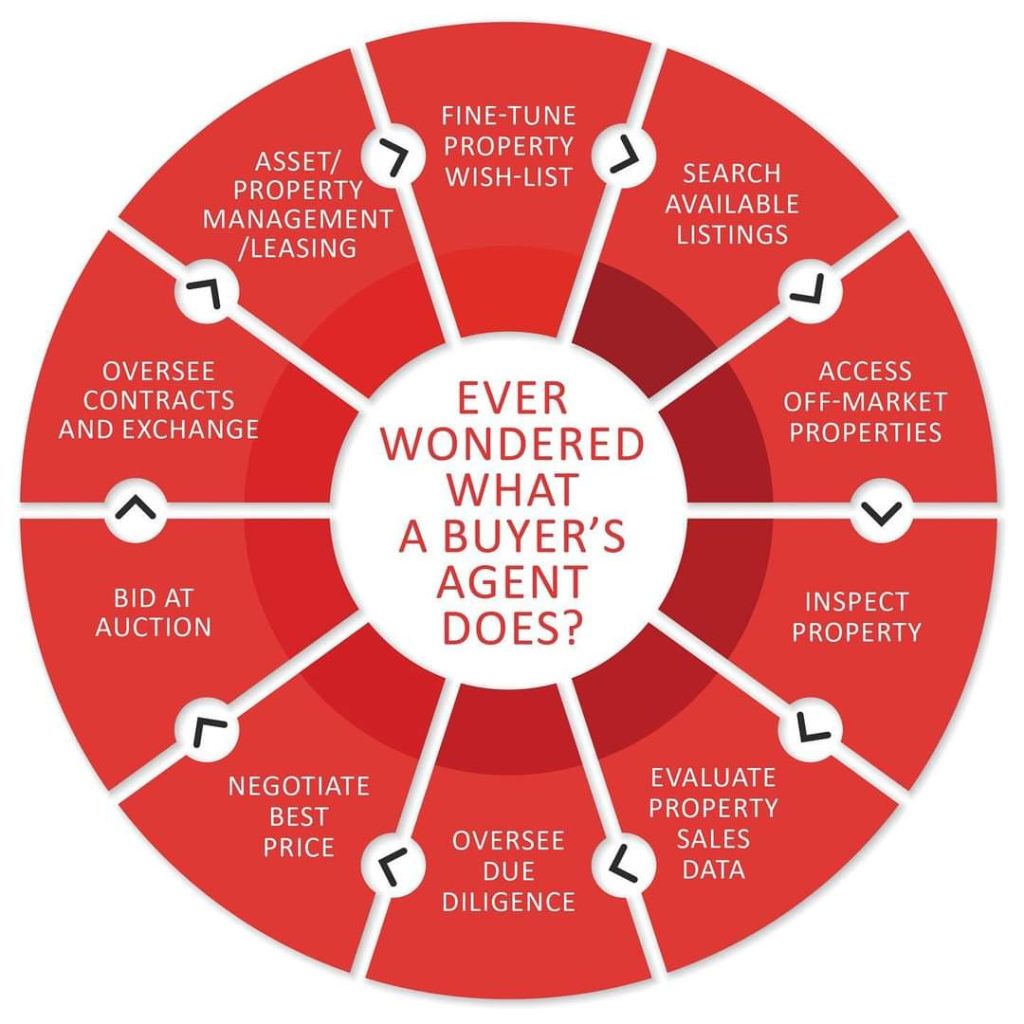

A truly experienced independent buyer’s agent understands that good property decisions are not made from a headline, a suburb ranking or a tax pitch. They are made through disciplined interpretation of the property cycle, data, comparable sales, rental evidence, title due diligence, planning context, macro and micro location drivers, construction quality, land content, property type and buyer-specific objectives.

Above all else, a buyer’s agent acts independently in the purchaser client’s best interests. Their role is to assess property through a broad and objective lens, aligned with the client’s criteria, budget, preferences and long-term goals. This includes providing informed recommendations based on experience, conducting property selection across the full available market – both on-market and off-market – and using professional networks to identify the best possible match. A truly independent buyer’s agent does this without preference toward any particular sales agency, vendor, builder, developer or pre-selected stock list, while actively avoiding conflicts of interest with sellers, referral partners and any existing client briefs or criteria.

The role of an independent buyer’s agent is not to pretend to be every adviser. It is to coordinate a well-rounded due diligence pathway and, where required, recommend that the client engage their own trusted, independent specialist advisers before purchasing.

That may include independent town planners, builders, building and pest inspectors, mortgage brokers, financial institutions, financial planners, solicitors, conveyancers, accountants, quantity surveyors, strata specialists, engineers or other technical professionals relevant to the property and strategy.

In some circumstances, where a client does not already have preferred professional advisers, a buyer’s agent may make impartial recommendations from a trusted panel of independent third-party advisers and relevant specialists. The panel should always include two or more options, allowing the client to make their own enquiries, consult directly with each adviser before engagement, and form their own independent decision.

This is how precise due diligence and well-strategised transactional decisions are implemented with confidence: the right adviser, for the right question, at the right stage of the purchase process.

Questions every buyer should ask before appointing a buyer’s agent or property adviser

- Are you licensed to act in the state or territory where the property is being purchased?

- Are you qualified and legally permitted to provide the specific advice you are giving?

- If you are commenting on tax, finance, credit, SMSF, legal, accounting or financial product matters, what licence or professional qualification authorises you to do so?

- Who is the licensee in charge, officer in effective control or responsible licensed person supervising the work?

- Will a properly licensed local agent or representative physically inspect the property and surrounding market?

- Are you paid only by me, the buyer, or do you receive any payment from sellers, developers, builders, sales agents or referral partners?

- Do you sell property, advertise property for sale, represent developers or receive stock from project marketers?

- Are you, or any allied referrer connected to this transaction, permitted under your licensing and professional obligations to receive commissions, rebates or referral fees?

- Will you provide a certificate of currency for professional indemnity insurance?

- Will you provide a written conflict-of-interest declaration and a rebate, referral fee and commission disclosure statement?

- Will you provide comparable sales, rental evidence, vacancy risk, suburb demand, planning context, title due diligence, construction quality, land-to-asset ratio and future supply analysis before recommending a purchase?

- Is the recommendation based on a broad market search or a limited panel of pre-arranged stock?

- Will you advise me not to buy if the property does not stack up?

New build and off-the-plan property: not wrong, but never automatic

Brand-new and off-the-plan property can have a place in a balanced strategy for the right buyer, in the right location, at the right price and with the right due diligence. New supply is important. Good construction matters. Well-located new homes can serve owner-occupiers and investors well.

But buyers should be cautious when new build is presented as the automatic answer to tax reform. The risks must be tested: land-to-asset ratio, developer margin, comparable established value, settlement valuation risk, construction timing, builder solvency, defects, warranties, owners corporation or strata costs, rental depth, future competing supply and resale appeal.

The more tax benefits become the headline, the more carefully buyers should interrogate the underlying asset.

The role of accountants, advisers and professional referrers

Allied professional advisers hold positions of deep trust. Accountants, financial advisers, mortgage brokers, lawyers and business consultants often know the intimate details of a client’s financial life. That trust should never be used as a shortcut into a conflicted property sales funnel.

A referral should be transparent, documented and in the client’s best interests. If a referral partner is being paid, the client should know. If the property provider is paying the adviser or referrer, the client should know. If the buyer is being directed only toward properties that generate a commission for the adviser network, the client should know.

In property, silence around the money trail is not a minor administrative issue. It goes directly to independence, motivation and trust.

If you are unsure, seek independent guidance before you buy

If you are unsure which way to go, or you are trying to navigate the noise in the property market, consider seeking a free, no-obligation independent consultation with a REBAA-accredited buyer’s agent before you buy.

An experienced independent buyer’s agent should help you slow the process down, test the evidence, understand the risks, challenge assumptions and identify which specialist advisers should be involved before you commit your capital.

Know the players in the game

Property decisions involve serious money, long holding periods and life-changing consequences. Buyers should slow the process down, ask better questions and insist on full transparency.

Before acting on property advice, know who is advising you, who is paying them, what they are licensed to do, whether they are insured, whether they are independent and whether the evidence supports the recommendation.

In a changing market, the strongest strategy is not panic, hype or tax reaction. It is calm due diligence, clear governance, disciplined asset selection and advice that is paid for by – and loyal to – the client.

Know the players in the game. Follow the money. Then decide whether the advice is truly working for you.

Author note

This article is intended as general consumer awareness commentary only. It is not legal, tax, financial, credit or personal investment advice. Buyers should seek advice from appropriately qualified and licensed professionals before making property, tax, financial, lending or structuring decisions.

Kind regards,

MASTER ADVOCATES – REAL ESTATE SERVICES Est. 2014

Mark Errichiello

Director, Co-Founder, Licensed Estate Agent, CEA (REIV), DipPropServ (Agency Mgt), REIA Diploma of Associate (AREI), (MAICD)

Independent Buyers & Vendors Advocate | Investment Property Management Advisor

– Elected REIV Board Member (Real Estate Institute of Victoria)

– Accredited Member REBAA (Real Estate Buyers Agents Association of Australia)

– Member PIPA (Property Investment Professionals of Australia)

M: 0408 988 118

Master Advocates + Byron Property Search

Residential and Commercial Advocacy

“Two generations strong. More than 45 years of combined real estate experience between the founders of Master Advocates. Over a decade of independent buyer and vendor advocacy. The Errichiello family legacy continues through Master Advocates – built on trust, strategy, service and lived property expertise.“

Your single point of personalised service and accountability – led by Mark & Michelle Errichiello, in collaboration with Michael Murray and the Byron Property Search team – supporting clients across key East Coast markets in residential and commercial property.

Where we serve:

• Victoria: Melbourne (Northern & Western specialists), Metro, Coastal & Regional — Victoria-wide

• New South Wales: Byron Bay, Byron Shire, Northern Rivers, Hinterland & Far North Coast

• Queensland: Brisbane, Gold Coast & South East Queensland (extended partner network)

Want a second opinion before you buy, sell, lease or sign anything?

Book a free initial consultation and we’ll help you clarify the best next step and offerings when it comes to comprehensive independent buyers agent purchase services, sale strategy, negotiation plan, or portfolio position

Websites

www.masteradvocates.com.au + www.byronpropertysearch.com.au

Consultation Booking:

https://calendly.com/masteradvocates

VICTORIAN GOVERNMENT AUCTION RESERVE PRICE DISCLOSURE LEGISLATION

Victorian Government Media Release and the REIV response

| COUNTER-PRODUCTIVE AUCTION RESERVE PRICE DISCLOSURE LEGISLATION IS RECKLESS AND WILL RESULT IN LESS TRANSPARENCY FOR VICTORIANS The Victorian Government has today introduced a Bill to Parliament to legislate reserve price disclosure seven days prior to auction. The REIV has respectfully engaged with Government over more than six-months to demonstrate the counter-productive nature of this legislation. We have done this through various channels: – a dedicated working group that presented comprehensive recommendations to support price transparency – one-on-one meetings with the past and the new Minister for Consumer Affairs – independent research to validate consumer feedback – media engagement – consultation with the department charged with developing the legislation and more. Unfortunately, the government has decided to progress this legislation irrespective of the evidence and information provided to the contrary. It is now important for Victorians to use their voices to make sure the government understands the impact of such legislation. Please see below links to: – a template letter that can be adapted to send to your local MP – the REIV media release – the REIV Blueprint for marketing residential real estate – The REIV urge all members and their clients and consumers to share this widely and help drive greater understanding of the impact of such legislation. Read the Victorian Government media release and the REIV response below to learn more. |